Five things to know about UK trade policy after the White Paper

We present the main points discussed by Professor L Alan Winters, Lord O’Donnell and Amar Breckenridge at a Trade Knowledge Exchange Webinar on 20 July.

A full recording of the session can be accessed here.

1. A grand political bargain

The White Paper is a negotiating text in two ways. Firstly, it sets out the UK’s offer to the EU, by building on previous statements made by the government, and also by responding to some of the positions set out by the EU in March of this year. Secondly, it reflects a painstaking effort at bridging divergent views within the government on the shape of future relation with the EU and with the rest of the world.

What is the political bargain that is proposed? Its main elements are as follows:

- To remain closely integrated to the single market on goods through the proposed Customs Facilitation Agreement and through partial regulatory alignment with the EU. This is intended to avoid causing disruptions to supply chains and to avoid a hardening of the Irish border. The quid pro quo for proponents of a harder exit was that this would allow, on paper at least, the UK to leave the EU customs union and negotiate free trade agreements with the rest of the world.

- Exiting the single market for services, in exchange for the UK being allowed to rescind single market principles around the movement of people. This confronts the EU’s stated position that the UK cannot selectively subscribe to some pillars of the single market and not others. The UK hopes that this might be negotiable, if it were to accept foregoing one aspect of the single market in exchange for opting out of another. This would also allow the government to meet one of its self-imposed red lines on control over its own migration policy.

Whether the political bargain will hold remains to be seen. Divergences within government seem to have hardened following the publication of the White Paper. This means that attempts to smooth the waters domestically have by and large dominated attempts to build bridges with the EU (an issue to which we return below). Setting these issues aside, how do the proposals stack up?

2. Goods: the devil will be in the detail

As observed above, the proposed Facilitated Customs Agreement and proposals for a “common rulebook” on regulation are the UK’s solution to the Irish border issue. It responds to the EU’s “backstop” proposal that would, in effect, implement a hard border in the Irish sea. This border issue must be solved in order for the Withdrawal Agreement to be finalised, and this in turn is a pre-condition for any negotiations on future arrangements (and for the transitional time period).

The proposals on customs and regulation also try to mitigate risks to cross-border supply chains that currently operate seamlessly within the customs union. Hence the words “as if in a Customs Union” that accompany the description of the FCA.

The FCA is not something that has been attempted before – in essence it is an attempt to recreate the operation of a Customs Union within the framework of a Free Trade Agreement (FTA) with the EU. Recall that the attraction of moving to an FTA is that it would allow the UK to strike deals with the rest of the world. But a regular FTA entails putting in place rules of origin between the UK and the EU, to determine eligibility for preferential treatment. This is important, notably for intermediate goods imported from third parties that are processed by UK firms that export to the EU. Such rules tend to add the cost of trade.

One reading of the FCA proposal is that it would do away with the need for rules of origin between the UK and EU altogether, with all administrative functions performed at the point of entry to the UK (as is the case now). These administrative functions would be complicated: imported intermediate goods would need to be tracked within the UK. The costs of these functions are supposed to be mitigated by a combination of technology and predictability in trade flows. Whether that will actually will be the case is far from clear. In practice, an increase in compliance costs seems inevitable, and the question is more on the locus of these: is it at the point of entry to the UK, or between the UK and the EU. The Irish border imperative means the government is more open to the first of these outcomes.

But setting that aside: other issues remain. In particular, the approach means that the UK would in effect apply EU tariffs to all intermediate goods that were then destined for EU via processing. If the UK were to apply lower tariffs, these would then be only on goods wholly meant for the UK. But if that is the case, that may reduce the attractiveness to third parties of negotiating a FTA with the UK. A similar observation might apply to the common rule book: regulatory alignment with the EU may limit the scope the UK has to accommodate partners with different regulation. This seems to be particular concern for trade with the US.

3. A different deal for services

In contrast to the position on goods, the UK proposes a more bespoke approach to services. The guiding philosophy seems to be that the depth of commitments – which are likely to be mainly around regulatory issues – will depend on whether alignment makes sense for the UK from an economic point of view, taking into account the options the UK might have of striking other deals with other parties. The UK’s position here may reflect its lower dependence on the EU for services relative to goods, and that this, in combination with its global clout, will put it in a stronger negotiating position. This probably explains the position on financial services, where having reminded the EU of the UKs strength in the sector, the paper calls for a specific agreement. It’s also worth noting that research suggests that in services, a country’s own liberalisation has a greater effect on its own exports than the liberalisation of trade partners. This might provide some support for worrying less about the effects of leaving the single market, particularly if UK-EU arrangements can be put in place in specific sectors.

As observed before, the approach to services is designed to allow the UK to leave the single market for services in exchange for allowing to exit commitments on free movement of people. However, exiting free movement comes with a cost: it is equivalent to putting up barriers to services trade by making it more difficult, for example, for firms to transfer employees or for individual suppliers to provide services by moving from one market to another. More generally, the ability to access skills and talent has been a key concern for various sectors, notably professional services, financial services and technology. The approach taken by the White Paper is to deal with issue of mobility by using the architecture of services trade (e.g. mode 4 commitments in GATS terminology). That would allow the UK, in principle at least, to (i) modulate its commitments on a sectoral basis depending on need (ii) remove the issue of access to skills and labour from the realm of migratory policy and access to national labour markets, and tie it to access to particular jobs in particular sectors. The approach also appears to do away with EU preference.

4. Will the bargain pay off?

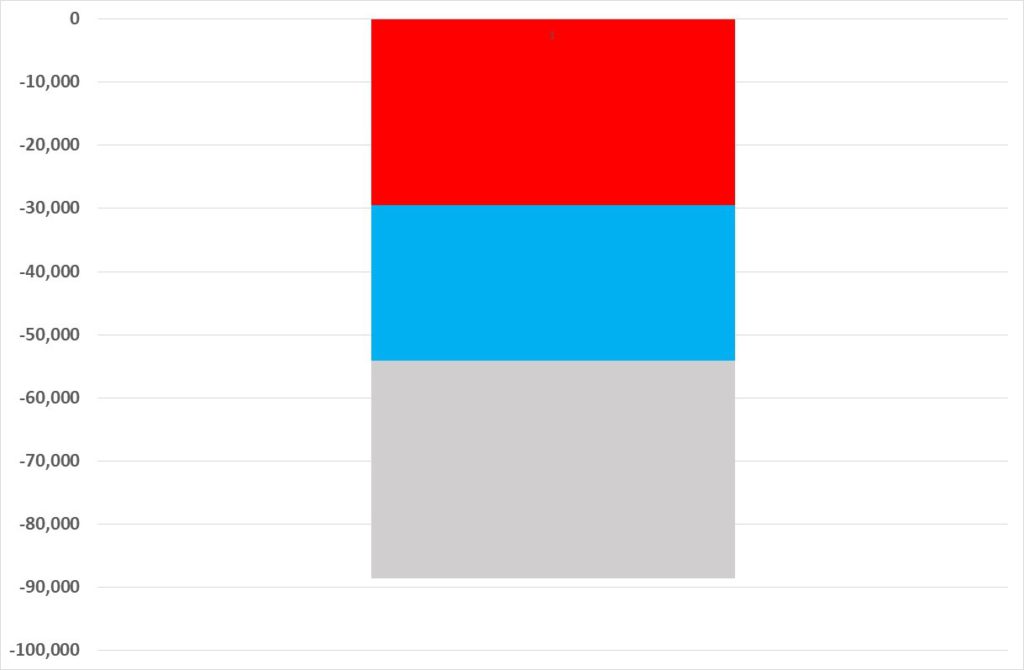

Figure 1 sets out the potential effects on exports of the UK moving away from away from the status quo. The red shaded area represents the effects of giving up single market access in services, and moving to a more conventional FTA agreement, and retaining a deep agreement in goods. The blue area represents the additional losses that come from moving to a Canada-style FTA on goods and services. The grey gives the additional losses from leaving without a deal.

These are rough numbers. The government would hope to reduce the extent of the red area by negotiating deeper commitments in services. But a failure to convince the EU that a Canada-style agreement is all that can be offered outside the single market would see the UK with the red and blue areas.

The other part of the equation is how the leaves the UK vis a vis the rest of the world. The White Paper’s strategy is to minimise the impact of moving away from current levels of integration with the EU while taking advantage of liberalising trade vis a vis the rest of the world.

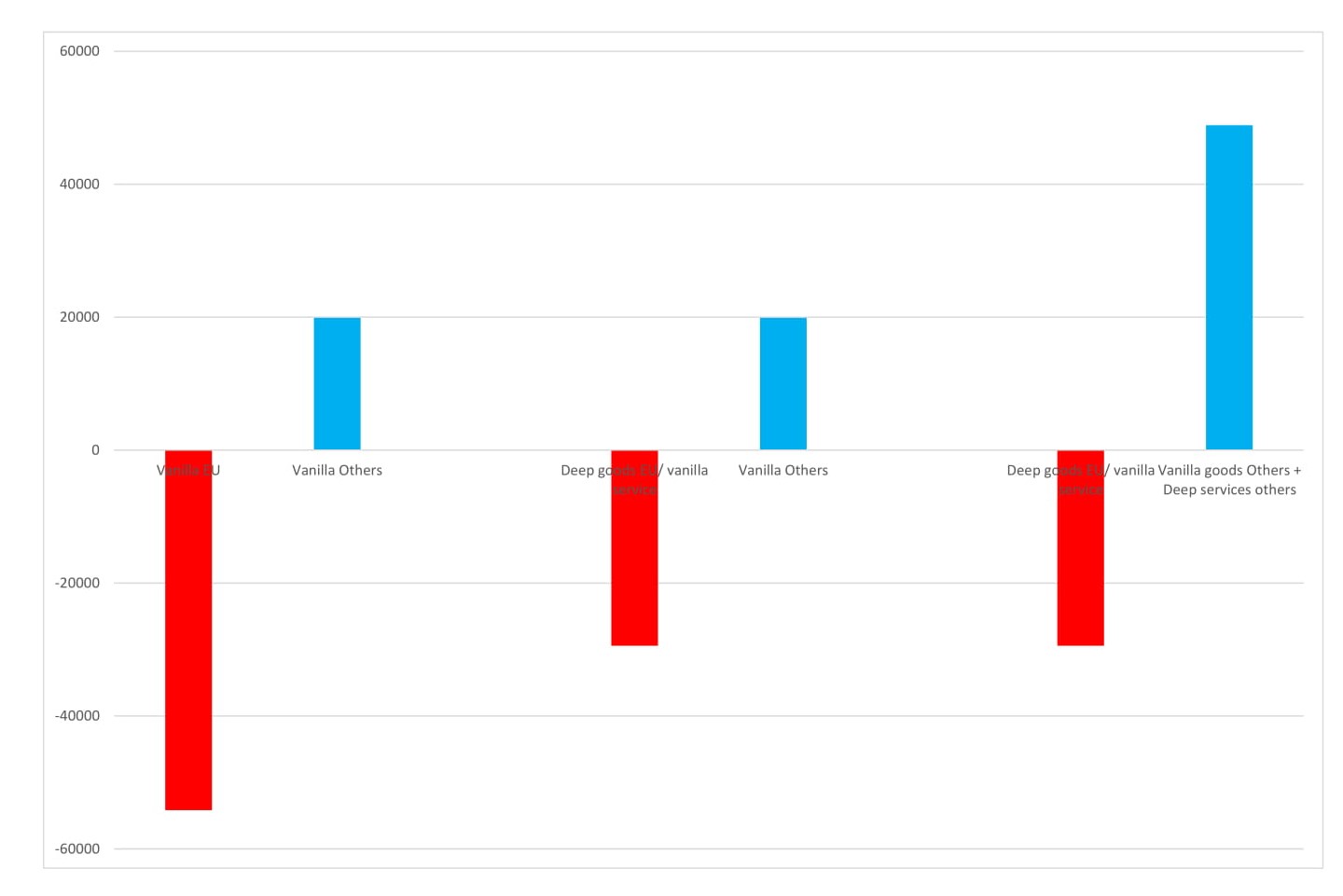

We can envision a variety of scenarios . As explained elsewhere, the main factor determining the effects of a FTA on trade is its depth. In Figure 2, we report results on the assumption that:

- The UK exits the EU and agrees a “vanilla agreement” (i.e. one that resembles the FTA the EU currently has with non-members, such as Canada) with the EU. The effects of this are represented by the left most red bar.

- The UK exits the EU, and negotiates an arrangement that has a deep FTA for goods and a shallower (“vanilla”) one for services. This is more consistent with the proposals in the white paper. The effects of this are reported in the second and third red bar charts.

- The UK signs vanilla FTAs with a number of third parties. This includes rolling over all existing FTAs to which it is already party via the EU, and concluding additional ones with the United States and Australia. The results are reported in the first and second blue bars.

- The UK rolls over all existing FTAs, and in addition negotiates deep FTAs on services with these partners. Goods trade remains at the “vanilla” FTA level.. The results are reflected in the right-most blue bar.

The results suggest that the deep goods/ shallower services approach of the White Paper would help to mitigate losses from exiting the EU. Signing FTAs with the rest of the world could offset, in part, or even outweigh these losses depending on the scenario. In the right-most blue bar chart, the biggest gains from deepening services liberalisation would come from the United States (around 80%). However, as we now explain, reaping these benefits will be a major challenge.

5. A fragile negotiating pathway

The White Paper’s proposals have been challenged both within government and by the EU. On the former front, amendments to the Customs Bill that in effect place duty collection obligations on the EU under the facilitated customs arrangement may make the latter unacceptable to the EU.

The EU for its part has expressed scepticism about the customs proposals, and more generally reiterated its insistence that the UK not “cherry-pick” aspects of the single market to which it wants to belong. Possibly coincidentally, the European Commission issued, in the week following the White Paper, a document explaining to member States the importance of preparing for a no-deal outcome.

The EU’s position that the UK must subscribe to all aspects of the single market rather than cherry-pick parts of it has been a long-standing position of the EU. As explained elsewhere, this a negotiating position, that has more to do with political factors than economic ones. The EU has a history of striking tailor-made arrangements and the White Paper can be seen as a call by the UK to the EU to conclude a pragmatic arrangement with a major partner.

As far as trade with the rest of the world is concerned, the main challenge for the UK is that negotiating and implementing “Vanilla” FTAs with the other major partners will take time. This is true even of agreements with existing partners like Japan and Korea that need to be rolled over.

Negotiating deep agreements with non-EU partners will be particularly challenging. In effect, this scenario assumes that the UK would be able to negotiate, at relatively short notice, levels of liberalisation not seen outside the EEA. In most of the UK’s major trade partners, conventional limitations on services (restrictions on foreign ownership, number of firms allowed to operate in a sector) are low or non-existent. Therefore services liberalisation is largely about regulatory reform and harmonisation. This would involve deep-seated policy reforms in both the UK and in the trade partners concerned. The scope for this is highly uncertain for various reasons. It is not clear that such liberalisation could be done on a preferential basis. Optimal regulation and public policy is context specific – reflecting social preferences to risk – and policy makers in the UK may not wish, for example, to align themselves more closely to approaches followed in the US.

Finally, as we have argued elsewhere, the attractiveness to trade partners of FTAs that focus primarily on services is unclear, especially given the UK’s global strength in services. Partners are likely to seek commitments in goods, but the scope and attractiveness of these may be affected by the common rulebook approach and uncertainties about how customs arrangements and rule of origin would operate.