Reflecting on the Challenges Facing UK Firms: Trade and Supply Chains

The UK left the EU in early 2020, and then entered into a new set of arrangements under the Trade and Cooperation Agreement at the start of 2021. There have been no shortage of studies on the impacts of moving to these new arrangements. Moreover, since the UK left the EU, it has had to context with a variety of other shocks – Covid-19 and its aftermath, supply chain shocks, and geopolitical tension sparked by the war in Ukraine. Most follow one of a range of macro-economic modelling approaches (thus, the OECD or the Office for Budget Responsibility on Brexit, or the IMF on the costs of economic fragmentation drawing on trade and other economic data.

An alternative is to quantify the experiences of businesses engaged in trade. This is the approach taken in a report by the UK Trade Policy Observatory (UKTPO ), in collaboration with the British Chambers of Commerce (BCC). It sheds light on the challenges faced by UK businesses, arising from the UK-EU Trade and Cooperation Agreement (TCA) and wider economic headwinds (Covid-19, Ukraine conflict), as well as firms’ concerns regarding their supply chains. They analysed over 2,800 sentences from the free-text responses to three British Chambers of Commerce trade-focussed surveys conducted over 2021 and 2022, which asked UK firms to report directly on these issues. From the findings, it is evident that over the last two years there have been significant hurdles for firms, ranging from increased costs and supply chain shortages to red tape and bureaucracy. In this article, we reflect on these insights and consider the potential impact on UK businesses.

Enduring The Headwinds

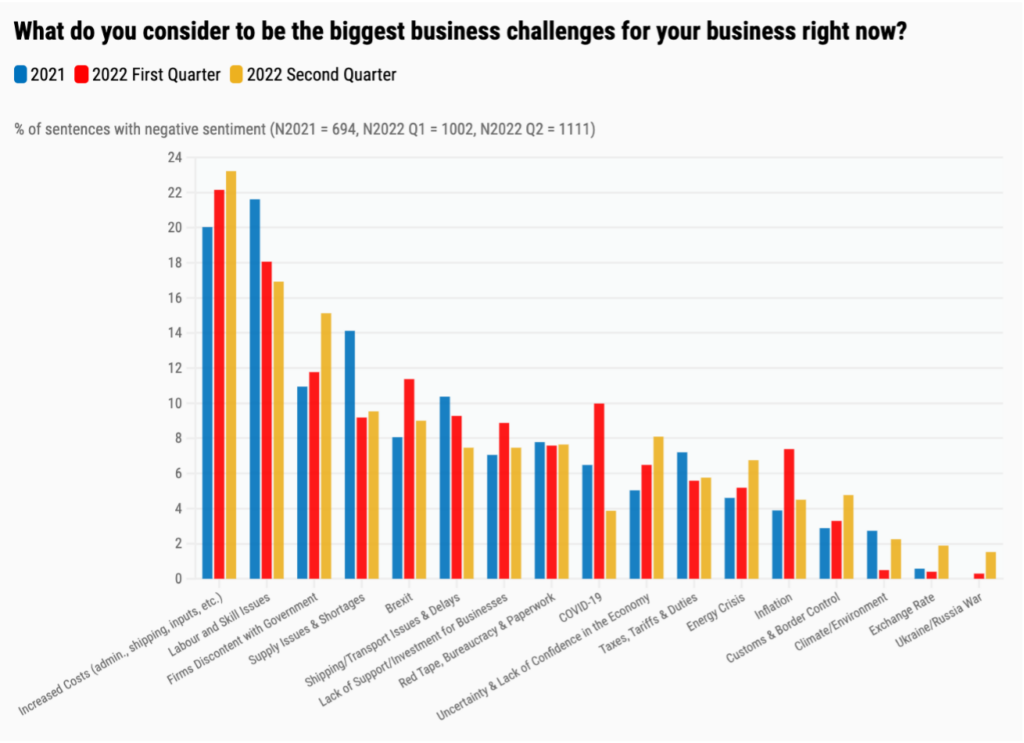

Unsurprisingly, the most prominent challenge is the issue of increased costs – this could be referring to costs of any kind, for instance raw material costs, energy costs (likely attributed to the Russia-Ukraine conflict), labour costs or shipping costs. Rising costs can severely impact businesses – affecting their profitability and their ability to stay in business altogether, especially in the face of competition from firms in countries not experiencing such cost increases. Furthermore, in response to such cost increases, firms are likely to pass these on in the form of increased consumer prices. Given that the UK is already experiencing a cost-of-living crisis, further price increases serve to exacerbate this issue.

Firms also report strong concerns surrounding labour and skill issues – whether that be labour shortages, issues with retaining labour or sourcing the appropriate skills – and express increasing discontent with the current government and government policy. UK businesses feel that current policy is not adequate to support their business activities and responses mention they feel unheard or ignored. Without the appropriate policy infrastructure to support enterprise, the productivity, growth and potential of UK businesses are constrained.

Although Brexit, the Covid-19 pandemic and the Russia/Ukraine conflict appear further down the list than one might expect, it is not to say that they have had little impact. It is important to consider how the effects of these shocks manifest. For instance, with Brexit, came the end of the free movement of labour and goods, and with covid-19 came (temporary) border restrictions and isolation requirements – both affecting the availability of labour and disrupting supply chains – which are both clearly significant issues for firms from our findings. Further, all of these complications increase costs for businesses – which we find to be their most prominent challenge. Many of the challenges reported by businesses are interrelated and the effects of one feed into another.

Have some suffered more than others?

For the latest survey data, the report reveals a higher intensity of challenges amongst certain industries, namely public administration, agriculture and manufacturing. Given the challenges firms have had to contend with, it is important to be particularly wary of the impact on firms involved in agriculture. For instance, as mentioned earlier, firms have been struggling with labour shortages, which is a critical input in the agriculture industry. Many agricultural businesses rely on seasonal workers, typically from EU countries, to meet peak labour demands during crucial periods such as planting and harvesting. These shortages can significantly impact the productivity of agricultural businesses, leading to reduced crop yields, difficulties meeting demand, and consequently impacting the livelihoods of UK farmers. Needless to say, the same may apply to many industries, but is particularly critical for the agriculture sector and may also impact on food security. Labour shortages may be one of the factors contributing to a higher negative sentiment reported by firms in the agriculture industry. Interestingly, amongst supply chain issues, labour was the most frequently reported services shortage, and the second most frequently reported shortage across goods and services overall.

We also find that these issues are widespread across the country. We don’t see much in the way of regional differences or differences by firm size – and this is perhaps surprising. Given the aggressive nature of so many consecutive shocks – the Covid-19 pandemic, the Ukraine-Russia conflict, the energy and cost-of-living crises, as well as the persistent complications of Brexit – one might have expected a more intense expression of negative sentiment amongst smaller firms, as it is often said that it can be more challenging for smaller firms to cope with these shocks and turbulences.

Grappling with the TCA

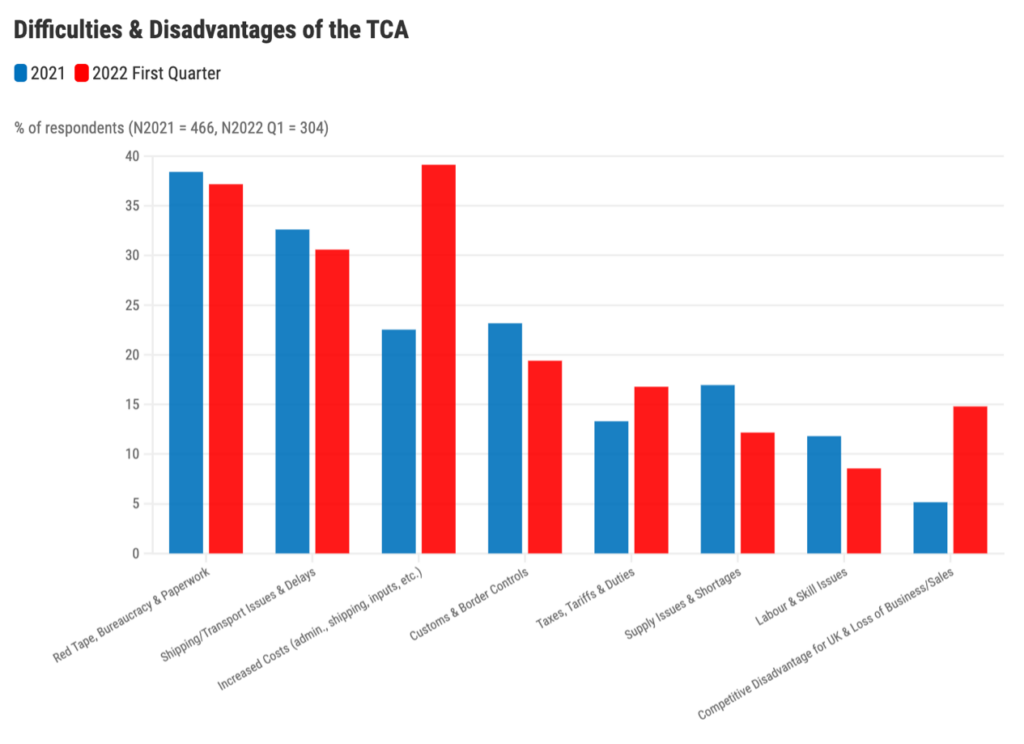

Another crucial issue is the impact of the TCA trading arrangement with the EU. Results show that UK businesses have been grappling with red tape, bureaucracy, and paperwork; increased costs; shipping issues and delays; and relatedly customs and border control complications. These factors have created additional complexities and burdens for UK firms who, and for firms who want to, engage in trade with EU partners. Firms now have to spend more time on unproductive activities to maintain existing business with partners in the EU and this is likely to deter new transactions. Businesses in the EU face the same challenges in wanting to trade with UK firms, but they have other EU firms on their doorstep, with the opportunity for much less burdensome transactions. Thus, intra-EU trade is likely to increase, whilst trade diverts away from UK business. Relatedly, for the latest survey by the BCC, we look at supply chain challenges specifically. Of the firms experiencing shortages (50%), over a third of these firms attribute the cause of such shortages to Brexit. The complications of our current trading arrangement with the EU are restraining opportunities with international partners and are likely to be putting UK firms at a competitive disadvantage.

Is there hope?

Firms were also given the chance to report their views on what they consider to be the biggest opportunities for their business. These were scarce. We found that 94% of all the sentences we analysed across the three surveys were of negative sentiment i.e., reported challenges, and only 6% of positive sentiment i.e., reported opportunities. This is a staggering asymmetry. While we may be innately hard-wired to focus on the negative – it is a survival instinct – nevertheless, this asymmetry in responses clearly reflects the pressures of the current economic climate faced by firms. Before even conducting any formal analysis of the data, simply reading the responses was a salutary reminder of the apparent relentless struggle that enterprise in this country seems to be facing.

The survey responses report a fairly bleak set of circumstances for UK businesses, and their consequent impacts underline the importance of the need for policy infrastructure by governments built on national consultation. Firms should be able to identify their concerns and feed them into policy-making decisions effectively to make sure policy is representative of what industry wants and needs collectively. Maintaining good trade relations will play an important role in meeting the needs of UK industry in negotiations across the world and, specifically, in dismantling the barriers with our closest and largest economic neighbour, the EU. The Windsor Framework, concluded in February 2023, is a step in the right direction to enhancing that trade relationship, but there is considerably more work to be done.