The European Union’s Carbon Border Adjustment Mechanism (CBAM) enters its initial transition phase in October 2023. The measure is part of the EU’s Green Deal and “Fit for 55” policy package, which aims to reduce Greenhouse Gas (GHG) emissions by 55% by 2030. Like many measures implemented in a “second-best” policy environment, it raises a number of complex issues. We consider these and the CBAM’s economic effects on the EU and partners.

The CBAM – what and why?

The CBAM’s primary declared purpose is to address the issue of “carbon leakage”. This arises when cross-national differences in GHG reduction commitments leads to the relocation of economic production from countries with more stringent reduction commitments to less stringent ones. If the relocation fails to lower global emissions while leaving countries with more stringent reduction commitments saddled with the economic costs of their commitments, then the outcome is economically inefficient. There are higher costs, but no environmental benefit.

How big an issue is carbon leakage? Evidence is mixed: to the extent that it occurs, it seems not to occur on a 1 for 1 basis i.e. the increase in emissions in less stringent locations is often found to be lower than the reduction in more stringent ones[1]. Though it could be argued that the incidence of leakage may increase as emissions price increase.

Setting aside carbon leakage, the motivation for CBAM seems also to be grounded in political economy concerns. Sectors that are emissions intensive fear that they will lose competitiveness and market share because they are undercut by rivals in jurisdictions with less stringent climate policies. In the EU, this concern dovetails with concerns about the effects of rising energy costs on industrial competitiveness. Over the last two decades, the EU has had low energy costs due to a combination of energy market liberalisation in a time of overcapacity, and large subsidies to renewables. Tightening supply conditions, combined with a tightening of environmental targets, have led to concerns that various sectors such as iron and steel could relocate elsewhere, and take with them co-located downstream activities (such as car making). These industries have generally been seen as “strategic” and all the more so at a time of geopolitical tension. It is also feared that the potential for disruption feared could undermine political support for ambitious reduction commitments.

Both carbon leakage and competitiveness issues could be addressed by mechanisms other than border adjustment. Historically, the EU dealt with the issue through “shielding” i.e the free allocation of permits tied to emissions intensity and output. Shielding is less efficient economically than border adjustment measures. Shielding requires more of the abatement task to be shouldered by non-shielded activities, whereas border adjustment spreads the task more broadly. Border adjustment is more environmentally efficient since emissions and output of emissions intensive sectors are lower than under shielding.

Moving away from domestic policy considerations to international ones, CBAM could be seen as a way to induce trade partners to undertake more ambitious emissions reduction commitments, and specifically to implement an explicit emissions pricing mechanism, as this would reduce their exposure to the mechanism. That in turn could enable global progress towards stabilising atmospheric concentrations of GHGs.

How would the CBAM work?

The CBAM in its current form is intended to equalise the tax on emissions faced by specific EU and non-EU products in EU markets[2]. The tax is determined by the emissions (direct and indirect) embodied in the products in question, and the prevailing price on emissions under the EU ETS. For any product, we can estimate an ad valorem duty by multiplying the emissions price by quantity of emissions and dividing by the value of imports. Seen this way, the CBAM acts in the same way as a tariff on imports. But unlike standard tariffs, it will fluctuate depending on the prevailing EU ETS price, and will vary by partner depending on the emissions intensity of their production.

The product coverage of the CBAM is likely to vary over time. The initial scope is Iron & steel, aluminium, fertilizer, cement, hydrogen, electricity. The scope may expand in the future to include organic chemicals and selected downstream products, such as other metals electrical goods, equipment and machinery, and food products.

CBAM targets differences in emissions prices, rather than differences in GHG reduction ambitions per se

A key point to note is that that the CBAM in its proposed form corrects differences in emissions prices or charges, rather than differences in GHG reduction targets per se. The distinction is subtle but important. It is possible to pursue GHG reduction targets without a market-based mechanism which either prices emissions through a trading scheme or through a flat price. [3] Non-market alternatives include regulation, moral suasion and subsidies on green investment. Indeed the approaches are necessary to address the market failures associated with decarbonisation, and will be required in addition to an emissions price. But many jurisdictions may prefer non-market approaches as alternatives to an emissions price, for a variety of reasons. (Some of these may be technical, particularly in less advanced countries; in industrialised countries, obstacles seem primarily political in nature).

If the EU’s concern were about carbon leakage, then it is differences in GHG reduction targets, not differences between formal pricing mechanisms that would be its focus. Instead, given what we currently know about the CBAM, a country may have a GHG reduction target that is close in ambition to the EU’s, but its products will be treated the same as a country with a much lower level of ambition if it lacks a formal mechanism for explicitly pricing emissions.

In principle, one could compute shadow emissions prices for all countries based on their abatement target (which gives the demand for abatement) and the costs of their abatement opportunities (which gives their supply curve for abatement). In practice, this would be complex, and the underlying modelling requires a range of assumptions around which there is unlikely to be consensus. A formal emissions price is a more visible reference point.

The CBAM as a way of mitigating the distributional effects of emissions pricing, and its political economy consequences

Setting aside complexity issues, the use of a formal emissions price as a reference point highlights that what the CBAM is targeting is the distributional impacts arising from different approaches to GHG reductions. As observed, worries about differences in cross-national emissions prices are concentrated in a handful of emissions intensive sectors that compete on global markets, and that are strategically sensitive. Under emissions pricing, these sectors incur resource costs associated with new technologies that will reduce emissions, and/ or on-going costs on their unavoided emissions (that are subject to the emissions price). Rivals not facing an emissions price could avoid these particular costs. That would be true even if those rivals operated in a jurisdiction which had relatively ambitious targets but pursued these by other means. Indeed, if that jurisdiction pursued abatement via large scale investment subsidies, then these rivals would be at a cost advantage.

In that case, why not simply ditch emissions pricing? The reason is that for the economy as a whole, emissions pricing is in principle more efficient. It prices an externality directly, and it relies on the price mechanism to send signals across the economy as a whole. Investment subsidies and other non-market mechanisms are more piecemeal, require significant administrative effort, and perhaps above all, impose a greater economic cost. This reflects the cost of public funds i.e. costs that reflect the fact that subsidies, need to be financed by taxation that will distort savings and investment decisions (or by cutting spending in other areas), and regulations. By contrast, revenues raised by emissions pricing can be recycled – either to finance other forms of green investment or to cut general taxes.

In aggregate, therefore, economic performance under emissions pricing should outperform economic performance under regimes that rely solely on alternative non-market mechanisms. It is more that the structure of emissions pricing generates concentrated impacts that fall on particular (sensitive) sectors, which generate incentives for them to lobby for protection from these costs.

This in turn underscores the points made earlier about the political economy nature of the CBAM: it reflects policy (and political) sensitivities about the sectoral distribution of GHG reduction costs in a world of incomplete and asymmetric GHG reduction commitments.

Economic effects on the EU – a tax on exports

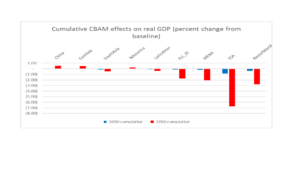

As is the case with standard tariffs, the main mechanism through which the CBAM’s effects play out are via changes to a the terms of trade and effects on relative prices. The two move in opposite directions for the EU. The CBAM improves the EU’s terms of trade, which in turn has a favourable, if limited, effect on its economic growth. At the same time, the CBAM increases the price of goods like cement and iron and steel that are primarily inputs into investment. This increases the cost of capital, which in turn reduces the capital stock, which reduces economic growth. Which of these two effects prevail depend largely on modelling sensitivities – in our modelling, the negative effects tend to prevail in the longer run.

What is clear, though, is that the CBAM reduces the EU’s exports. As the CBAM covers a limited range of sectors, it leads to a reallocation of resources to these sectors. It increases prices within the EU, making internal trade more attractive than external trade. The real exchange rate appreciation associated with improved terms of trade dampens exports generally. We thus have a paradoxical result that a measure enacted to safeguard the competitiveness of specific sectors has a negative impact on the EU’s external competitiveness. This result is largely in line with what we’d expect with standard tariffs: a tax on imports acts as a tax on exports.

Economic effects on EU trade partners

What of the EU’s partners? Again, the main transmission mechanism is via the terms of trade, and overall effects depend on a country’s underlying economic characteristics. For, China, which is one of the main targets of the CBAM, effects are actually relatively muted: as with the EU, they could vary from mildly negative to mildly positive. China faces high ad valorem CBAM duty rates which leads to a substantial fall in its exports of CBAM products. However, the real exchange rate depreciation caused by this fall boosts the exports of non-CBAM products, which attenuates (if not offsets) these impacts. Effects on India, and South Asia more generally, are more negatively affected than China.

The main negative impacts fall on Sub-Saharan Africa. Ad valorem rates on the region’s exports are high, and consequently terms of trade effects are also strong. The negative effects of real exchange rate depreciations boosts exports of non-CBAM sectors. But at the same time, both the negative terms of trade effects and the real exchange depreciation are associated with an increase in the cost of capital and reduction in the capital stock. Because Sub Saharan Africa is particularly labour intensive, a reduction in the capital stock has more pronounced productivity effects, and thus adverse growth effects.

Policy implications and responses

The structure and operation of the CBAM suggest that it is primarily a political economy instrument, operating in a second-best environment. Let us assume that it is required to shore up support for ambitious emissions reduction efforts within the EU. The EU and partners are better off with such ambitious efforts, compared to a world with weaker EU reduction efforts and no CBAM. As with any policy instrument in a second-best environment, the question is then how to manage the costs that inevitably come with it.

For the EU, the main issue is that a measure designed to preserve the competitiveness of specific sectors likely leads to a loss, albeit modest, of overall external competitiveness. That may mean that the EU requires further measures e.g. fiscal reforms within its members states, possibly supported by the recycling of CBAM revenues to offset the CBAM’s effects. Sectors that face increased input costs may also push for specific forms of support. The EU will need to decide for itself whether the overall political economy effects of the CBAM plus further measures are justifiable relative to not imposing the CBAM in the first place.

At a global level, the impacts of the CBAM are generally modest, including for emerging economies like China. This is because of the interplay of offsetting impacts. The terms of trade effects depress growth and real exchange rate depreciation effects will tend to increase it.

The economic impacts on Sub-Saharan Africa are the largest. Given that these countries are, on aggregate, the poorest and most vulnerable, it is important to consider what policy responses are appropriate . The CBAM’s transmission mechanisms – terms of trade and cost of capital- suggest several options. The first is to reduce trade costs faced by Sub Saharan African exporters. This is partly a question of improved market access to EU markets. But trade costs are also generated by factors within the region e.g. a lack of infrastructure; the export tax effects of import tariffs; and deficiencies in trade facilitation. Initiatives such as the African Continental Free Trade Area (and regional initiatives) could play a role. Shocks like the CBAM expose weaknesses in the domestic policy settings for trade. External support combined with domestic reforms could address these.

Possibilities for multilateral cooperation?

The structure of the CBAM could present partners with incentives to develop formal emissions pricing mechanisms, in order to limit CBAM tariffs. In that sense, CBAM could encourage a transition to more efficient forms of emissions reductions i.e. by using price mechanisms rather than relying solely on subsidies and regulation. The processes for measuring and reporting emissions could present opportunities for regulatory cooperation.

Finally, the CBAM is a new beast in the trade policy ecosystem. While it behaves in many ways like a standard ad valorem tariff, the underlying mechanisms that determine how it works are novel and untested. In particular, the processes for estimating, reporting and verifying direct and indirect embodied emissions is complex and fertile ground for disputes. This calls for transparency and monitoring, and the WTO would have a key role to play in that.

[1] See IMF 2021

[2] Strictly speaking, CBAM should also seek to equalise the burden of emissions taxation faced by EU exports in global markets, but this aspect hasn’t been settled yet.

[3] The EU-ETS is an example of a market based on capping the quantity of allowable emissions and allowing trade between emitters, with the price for emissions permits set by the market. An alternative is a flat carbon price, of the sort implemented by Australia between 2011 and 2013. Various variants exist, including trading based on emissions intensity baselines. See Frontier Economics Australia (2008) for a discussion.